Toward the Alberta Advantage:

Withdrawing from the Federal Corporate Income Tax Collection Agreement

Late in 1978 and early 1979, the Peter Lougheed government embarked on a mission to lower the "small business" income tax in Alberta. This move accompanied Alberta's withdrawal from a federal tax collection agreement, marking a significant milestone in what we now recognize as The Alberta Advantage. The historical context of Alberta's departure from the federal corporate tax collection scheme bears relevance to our present, particularly when considering parallels with the desire to exit the Canada Pension Plan (CPP).

I don’t typically write much about taxes, but during my ongoing exploration of the Provincial Archives of Alberta (PAA), I uncovered some documents that intrigued me. Ordinarily, the topic of tax reductions or tax anything might not make for exciting reading. However, the documents stood out for me because their context seemed in many ways similar to the present. Put differently, it’s the story that caught my eye and not the numbers, even if the numbers are also important. And if you're in my age group, speaking of stories, you might even recall what you were doing back in 1978-79, when Alberta's ministers were crafting a strategy to counter Ottawa's corporate income tax hikes.

Alberta's plan involved some friction with the federal government. Quelle surprise! By early 1979, Peter Lougheed had been premier for over 7 years and there had been no shortage of conflict, especially given the contentious energy-related issues, between Alberta and Ottawa. At the start of 1979, Alberta's Minister of Finance was Lou Hyndman, while Ottawa's was Jean Chrétien.

At that time, the federal income tax rate for small businesses stood at 20 percent, whereas Alberta's was at 11 percent. However, Ottawa, under Pierre Elliot Trudeau, hungry for more revenue intended to redefine the tax boundaries, effectively removing professional corporations like dentists and doctors from the "small business" category. This shift would have them paying a total of 47 percent income tax (36 percent federal and 11 percent provincial) starting in January 1980.

Changing the small business definition was being done to suit Ottawa's hunger and did not serve Alberta’s strategic goals. The Alberta government aimed to get ahead of this change to protect Albertans and their interests.

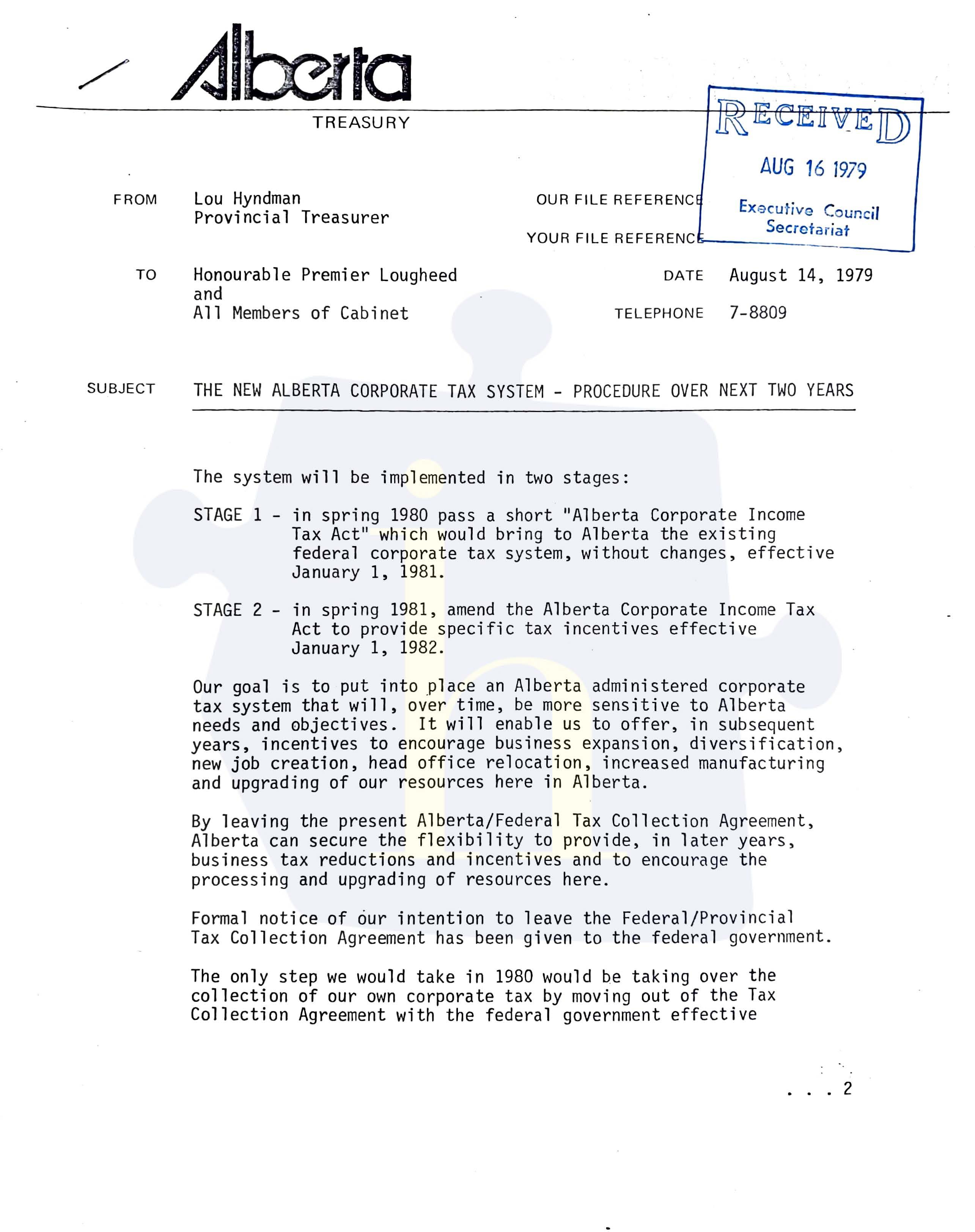

Rather than simply eliminating its 11 percent corporate income tax to cushion the blow for Alberta's small businesses, the provincial government chose a different path. It opted to overhaul its corporate tax regulations, assert its constitutional authority, introduce new legislation and exit the Federal Tax Collection Agreement.

"Our goal," wrote Hyndman in a memo to Lougheed on August 14, 1979, "is to put into place an Alberta-administered corporate tax system that will, over time, be more sensitive to Alberta needs and objectives. [...] to encourage business expansion, diversification, new business creation, head office relocation, increased manufacturing and upgrading of our resources in Alberta."

As fate would have it, Pierre Trudeau had already left office by the time that Hyndman memo was written in August 1979, and a new Alberta-born Prime Minister, Joe Clark, took office two months earlier on June 4th. However, documents indicate that Alberta's decision to exit the Collection Agreement was made before Clark's inauguration, indicating that the change in government did not alter Alberta's course.

The process involved serving notice to Ottawa about Alberta's intent to leave the Collection Agreement. Hyndman informed the premier in the same memo that it had been done. Alberta would be "taking over the collection of our corporate tax.... effective January 1, 1981,” necessitating the establishment of an "Alberta Corporate Tax Branch" within the Provincial Treasury, equipped to levy fines and adjudicate disputes.

Thwarting Ottawa's plan against small businesses initially required Alberta to slash its corporate "small business" income tax rate from 11 to 5 percent—a 55 percent reduction. Alberta also passed its own Alberta Corporate Income Tax Act. Starting January 1, 1981, this new Alberta law would essentially mirror the federal legislation "without changes." This meant that for the full year 1981, Alberta would live exclusively under the federal tax system. That strategy might be challenging for the Alberta government to sell today. The change was projected to cost the Alberta government $40 million in revenue, but it was expected to generate a $500 million boost in investment.

Back when media outlets covered this sort of thing, they covered Alberta's Business Tax reduction with keen interest, presenting a range of perspectives. Some hailed the tax reduction as a bold and innovative step that would attract businesses, stimulate economic growth, and create jobs. They emphasized the potential benefits, such as increased investment and competitiveness. However, not all news outlets were supportive, arguing that it could lead to revenue loss, potentially affecting public services or increasing taxes for individuals. These critics questioned the “fairness” of the tax cut, its impact on income inequality and the government's ability to fund essential services.

Lougheed's plan unfolded in two stages. First, Alberta adopted federal legislation into the Alberta Corporate Income Tax Act. In the second stage, during the Spring of 1981, specific tax incentives, effective from January 1, 1982, were introduced. These measures included reducing the provincial corporate tax rate for small businesses to zero percent, providing additional reductions for all businesses involved in manufacturing in Alberta, and reclassifying professional corporations as small businesses.

Keep reading with a 7-day free trial

Subscribe to Haultain Research to keep reading this post and get 7 days of free access to the full post archives.